|

SENIOR shipping executives

last year predicted that the container shipping

industry would see a rise in consolidation

in the years to come, and that the pool

of competition in the market would become

less crowded.

Now almost one year on from when we first

heard many of those projections, do we see

any signs that such an occurrence is happening,

or will happen in the not too distant future?

There are two schools of thought on the

matter. One school says that while the difficult

operating environment may claim the odd

casualty here and there, the liner landscape

going forward will not change any more than

it has in the past.

The other school is convinced that there

is a slew of mergers and acquisitions on

the horizon, and that tough times will result

in drastic measures, either forcing some

carriers out of the business altogether,

or force them to look to stay alive through

partnership.

To date, it would appear that the former

school of thought is more accurate. We have

not seen any major changes. There of course

have been some changes this year, and that

is what we will be looking at today…

To understand what has changed, we must

first see what the situation was heading

into this year.

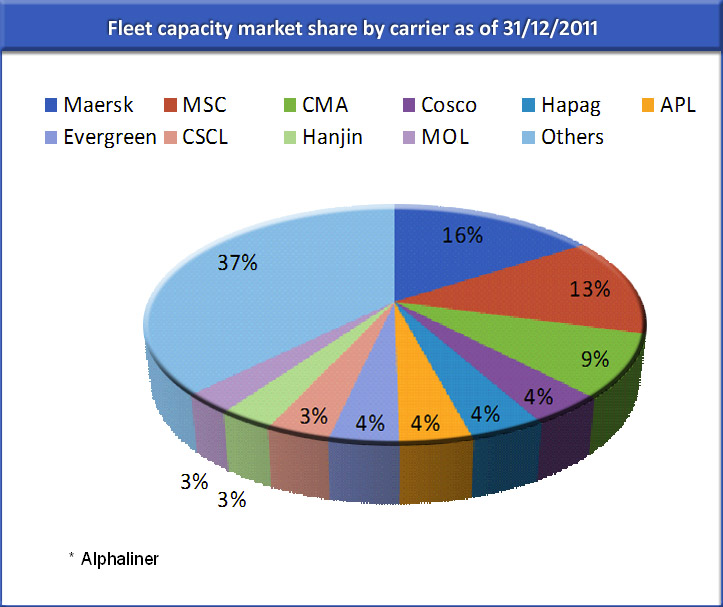

In the below pie graph we can see the

market share situation in terms of fleet

capacity as it stood at the end of 2011.

click image to enlarge

click image to enlarge

"Worldwide

container shipping capacity on December

31, 2011 stood at 15.89 million TEU, while

the number of container vessels in the market

numbered 4,919.

The twenty largest carriers then controlled

a combined market share of roughly 80 per

cent of the global containership fleet,

or 13.38 million TEU.

The top 10 carriers held a market share

of over 60 per cent at the end of last year,

headed by Maersk Line at 16 per cent, MSC

at 13 per cent and CMA CGM at nine per cent,

as shown in the above graph.

This makes for a combined market share

of 38 per cent for the top three shipping

lines in the world.

So what has changed between then and

now?

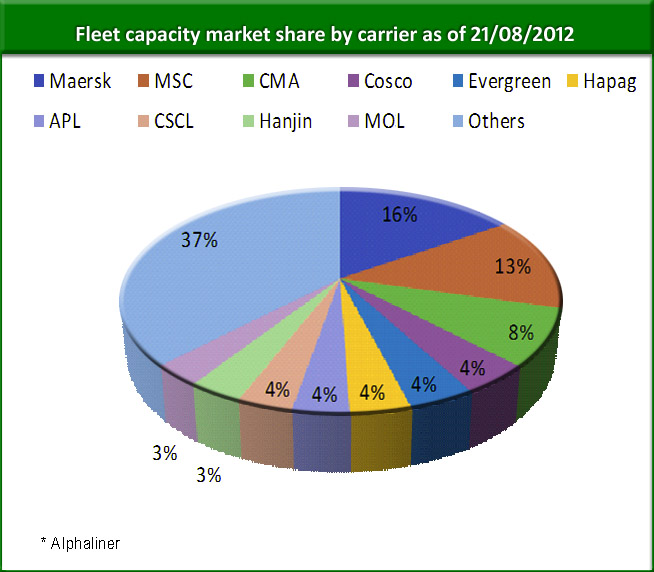

It would seem not much, judging from

the below graph.

click image to enlarge

click image to enlarge

The global fleet, as of August 21, has

changed in the sense that it has grown significantly.

The total amount of capacity has risen to

16.63 million TEU across 5,967 vessels.

This represents an increase of less than

five per cent since the end of last year.

The top 20 carriers now hold a market

share, in terms of available fleet capacity,

of 84 per cent. So it would appear from

that figure that the larger players are

growing larger in comparison to those lines

outside of the top 20, which in turn could

imply a move towards a smaller pool of competition

going forward.

For the top 10 carriers there appears

to be little change, however.

The market share for these lines remains

at 63 per cent. The only differences are

that CMA CGM’s share has slipped from nine

per cent to eight per cent and CSCL has

increased its share from three to four per

cent.

Page 1 2 [Next]

|