|

Page

3 of 3

After

2001 the industry experienced a number of

large mergers and acquisitions, which led

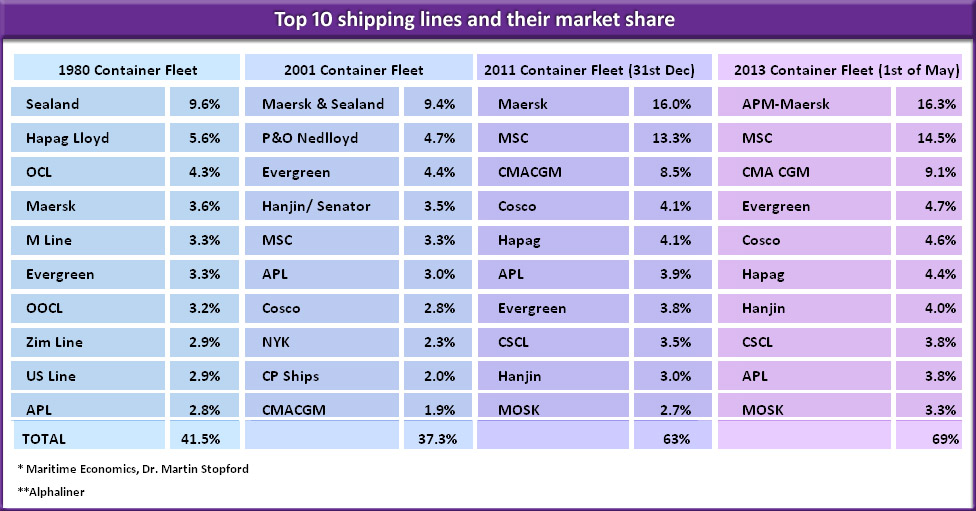

to a much less fragmented market. By the

end of 2011 the top 10 carriers held a market

share of 63 per cent, while the top three

carriers saw their share rise to 38 per

cent. This is a massive jump from a decade

earlier.

If

we then fast forward to the present, the

market concentration has increased even

further, despite the absence of mergers

and acquisitions.

The

top 10 carriers as of May 2013 now hold

69 per cent of the industry's market share,

while the top three have increased to 40

per cent. This is remarkable considering

there have been no mergers among the major

players.

In

other words, the container shipping industry

is undergoing consolidation, but it is consolidation

through asset expansion, not mergers. Therefore

it is much more subtle.

But

regardless of whether the consolidation

is subtle or overt, the end result will

be the same - fewer players that will continue

to control more and more of the market and

a significant reduction in industry competition.

The ultimate losers in this scenario

will be the shippers.

Let's

now see which players command the bulk of

the market share today.

click image

to enlarge click image

to enlarge

Clearly

Maersk Line is the leader. It has grown

its market share from 3.6 per cent in 1980

to 16.3 per cent today. This increase in

market share has been greatly helped through

mergers and acquisitions.

MSC

on the other hand, which has grown its market

share from 3.3 per cent in 2001 to 14.5

per cent has done so through the more subtle

approach - adding more and more ships to

its fleet. CMA CGM has also been a big mover

over the past decade, increasing its share

from 1.9 per cent in 2001 to 9.1 per cent

today.

Within

the top 10 players itself there is a fairly

even spread in terms of market share. However,

the three to watch going forward will be

Maersk Line, MSC and CMA CGM, which have

increased their shares so significantly

over the years, and continue to do so today.

Should

they grow much further it could become a

major challenge for the rest of the industry

to overcome, particularly on the Asia-Europe

and transpacific trades where only the biggest

carriers will be able to survive.

Page 1 2 3

|